By Bosstox Newsroom

After today’s Fed decision, the market did what it always does after the Fed stops being dramatic:

It started telling the truth again.

Not through headlines.

Not through speeches.

Through prices.

And right now the truth is this:

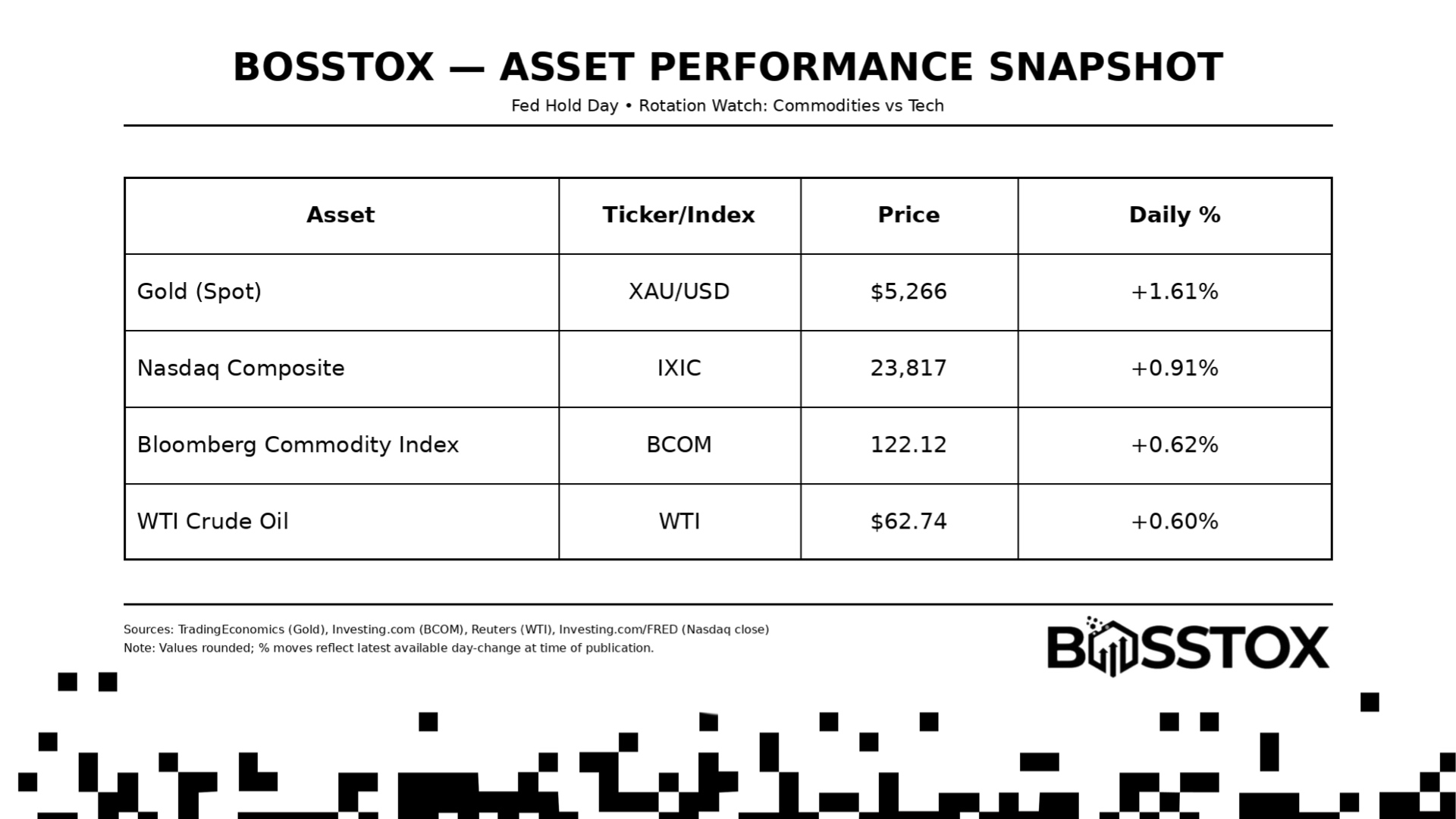

- Commodities are moving like inflation isn’t dead

- Market cap is acting like growth isn’t safe

- Gold is screaming

- Tech is bleeding

- and the overall market is whispering one word:

Reshift.

Inflation Isn’t “Coming Back” — It Never Fully Left

People keep saying “inflation might return.”

Bosstox disagrees with the framing.

Because inflation never vanished. It just changed form.

It went from:

- groceries + gas

to:

- insurance + labor + services + rent pressure + supply chain costs

Inflation doesn’t disappear.

It migrates.

And commodities are where inflation shows up first — not last.

That’s why commodities matter so much right now: they’re early-warning systems for what pricing power is doing across the economy.

When commodities spike, companies get squeezed.

When companies get squeezed, they cut.

When they cut, labor slows.

When labor slows, recession probability climbs.

So yes— commodities and inflation are directly linked.

But more importantly:

commodities and recession are linked too.

Market Cap = Market Confidence

Let’s talk market cap.

Market cap isn’t just a number — it’s the market’s collective vote on future stability.

When capital rotates away from mega caps (especially tech), the market is saying:

“We’re less certain about tomorrow than we were yesterday.”

That’s what we’re watching now.

The market is leaning into defense, not fantasy.

And the “dip” you’re seeing isn’t random:

It’s market cap re-pricing risk.

In plain English:

- big money is rebalancing

- institutions are cleaning portfolios

- and retail hasn’t fully realized the shift yet

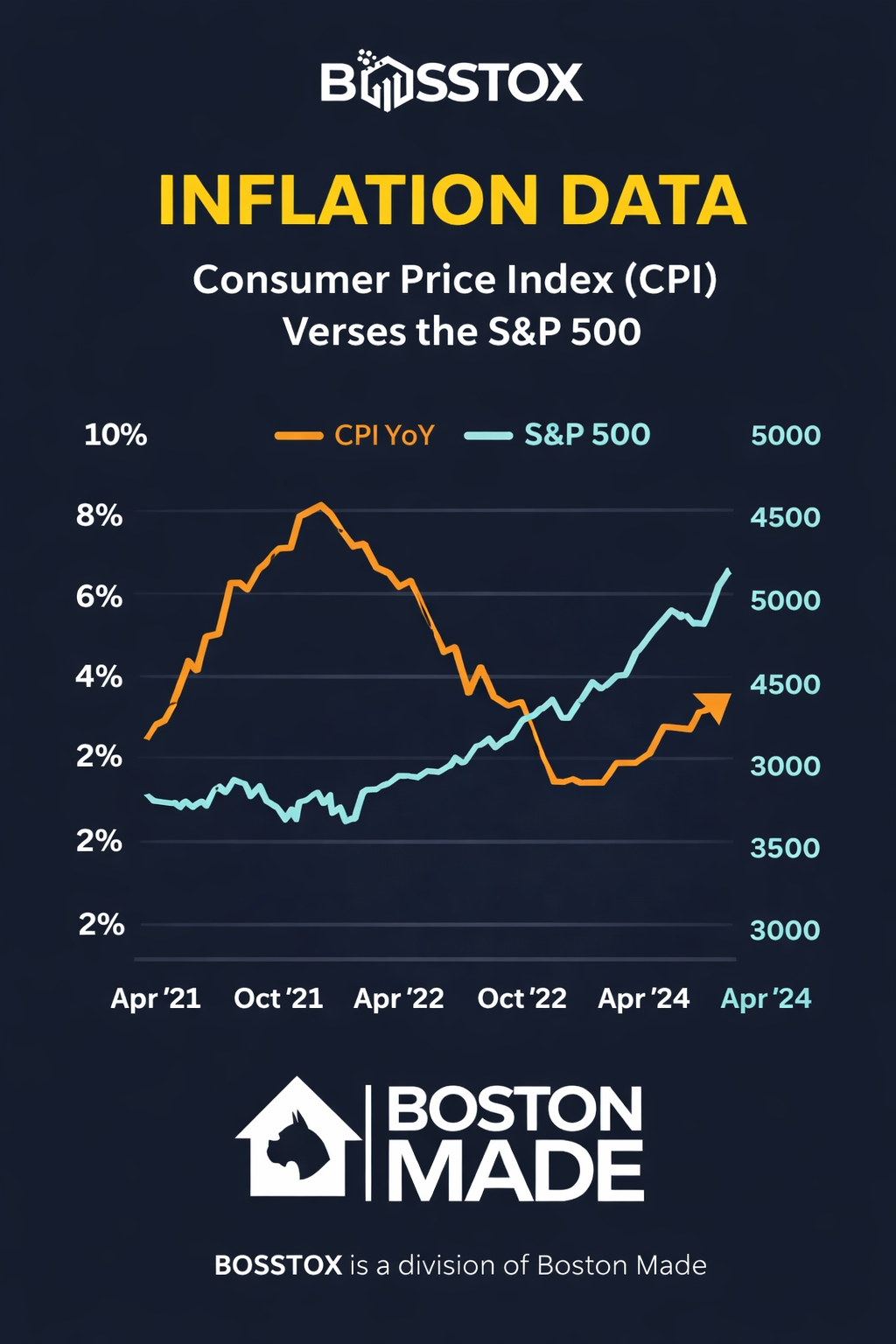

Gold at All-Time High While Tech Bleeds = The Loudest Signal in Finance

Read this slow:

Gold is at an all-time high… while tech is down.

That combination is not normal.

Gold tends to rise when:

- confidence drops

- currency weakens

- inflation pressure lingers

- global stability deteriorates

- recession risk rises

Tech tends to fall when:

- rates stay elevated

- liquidity tightens

- risk appetite shrinks

- future earnings get discounted harder

- market cap concentration becomes dangerous

So when gold is ripping and tech is slipping, the market is basically announcing:

“We don’t trust the future the way we did.”

That is not fear.

That is positioning.

And positioning moves the world.

Stocks Dipping While Commodities React = Stagflation Shadow

Here’s the danger zone Bosstox watches harder than anything:

- stocks weakening (growth fear)

- commodities staying strong (inflation pressure)

That mix breeds one monster:

stagflation vibes

Not necessarily stagflation itself, but the shadow of it.

Because if:

- pricing power stays elevated

- but demand starts slowing

then the Fed gets stuck in the worst possible setup:

✅ inflation isn’t low enough to cut fast

✅ growth isn’t strong enough to tolerate tight policy

✅ recession becomes possible without “relief”

That’s when mistakes happen.

And that’s when markets drop hard.

“It’s Time to Reshift” Isn’t a Motivational Quote — It’s an Institutional Directive

Let’s be blunt.

This is not the environment to blindly worship tech.

Not the environment to chase hype.

Not the environment to “buy the dip” like it’s 2021.

This environment is:

reshift season

A rotation.

A reorganization.

A corporate-level portfolio rewrite.

This is where capital moves like an army, not a lottery ticket.

That means we are likely to see:

- less concentration

- more value + commodity exposure

- more defensive allocations

- more money parked

- more restructuring

The Banker Closet: Why This Market Feels Like Reorganizing a Business

This week, the CEO of Boston Made spoke with a banker — and the banker said something that Bosstox won’t forget:

“The market is like a closet. Everything’s being pulled out, refolded, reorganized… and put back in a better place.”

That’s the best analogy for what’s happening in America right now.

Not collapse.

Not explosion.

Restructure.

Re-stack.

Re-label.

Re-file.

Rebuild.

Businesses are doing the same thing.

They’re not growing wildly.

They’re tightening.

Optimizing.

Creating space.

Repositioning teams.

Reducing waste.

Securing credit lines.

Rewriting supply chains.

Big Organizations Aren’t Moving Alone — They’re Moving Through Intermediaries

Here’s another Bosstox truth the headlines ignore:

Most organizations don’t restructure directly.

They restructure through:

- bankers

- lenders

- private equity

- consultants

- insurance intermediaries

- compliance + finance teams

- third-party administrators

- procurement pipelines

They don’t say “we’re weak.”

They say:

- “We’re realigning”

- “We’re optimizing”

- “We’re improving efficiency”

- “We’re undergoing a transformation”

But translation?

They’re preparing for a tighter world.

A more expensive world.

A world where:

- debt costs more

- consumers hesitate

- and profits must be defended

That’s why restructuring is everywhere.

Not just in small businesses.

In massive ones.

Bosstox Forecast (No Fluff): Inflation Risk + Recession Probability Can Rise Together

People think inflation and recession can’t happen together.

False.

They can rise together if:

- supply costs stay elevated

- labor cost stays sticky

- currency pressure increases

- and demand slows

That’s why commodities + market cap matter.

This is the scoreboard.

If commodities remain strong while the market dips, inflation isn’t “gone.”

It’s just changing shape while growth slows.

That is the condition that breaks confidence.

Final Word: This Is the Reorganization Economy

This is not the boom economy.

Not yet.

This is not the crash economy.

Not yet.

This is:

the reorganization economy

The economy where:

- portfolios get reshuffled

- businesses restructure

- credit becomes selective

- and winners are built in silence

So when you see:

- gold up

- tech down

- commodities reacting

- market cap rotating

don’t panic.

Don’t worship.

Reposition.

Because the closet is being reorganized.

And the people who understand that early…

are the people who come out dressed like kings.