In a series of sweeping economic claims, Donald Trump has once again put the global financial system on notice. At the center of his argument is a radical idea: defense companies operating across NATO-aligned countries should not be allowed to use capital for stock buybacks. Instead, that capital, he argues, should be redirected toward production, labor, domestic manufacturing, and border security.

Trump claims that under this framework, the stock market could ultimately double—not through financial engineering, but through forced reinvestment, territorial leverage, and geopolitical consolidation.

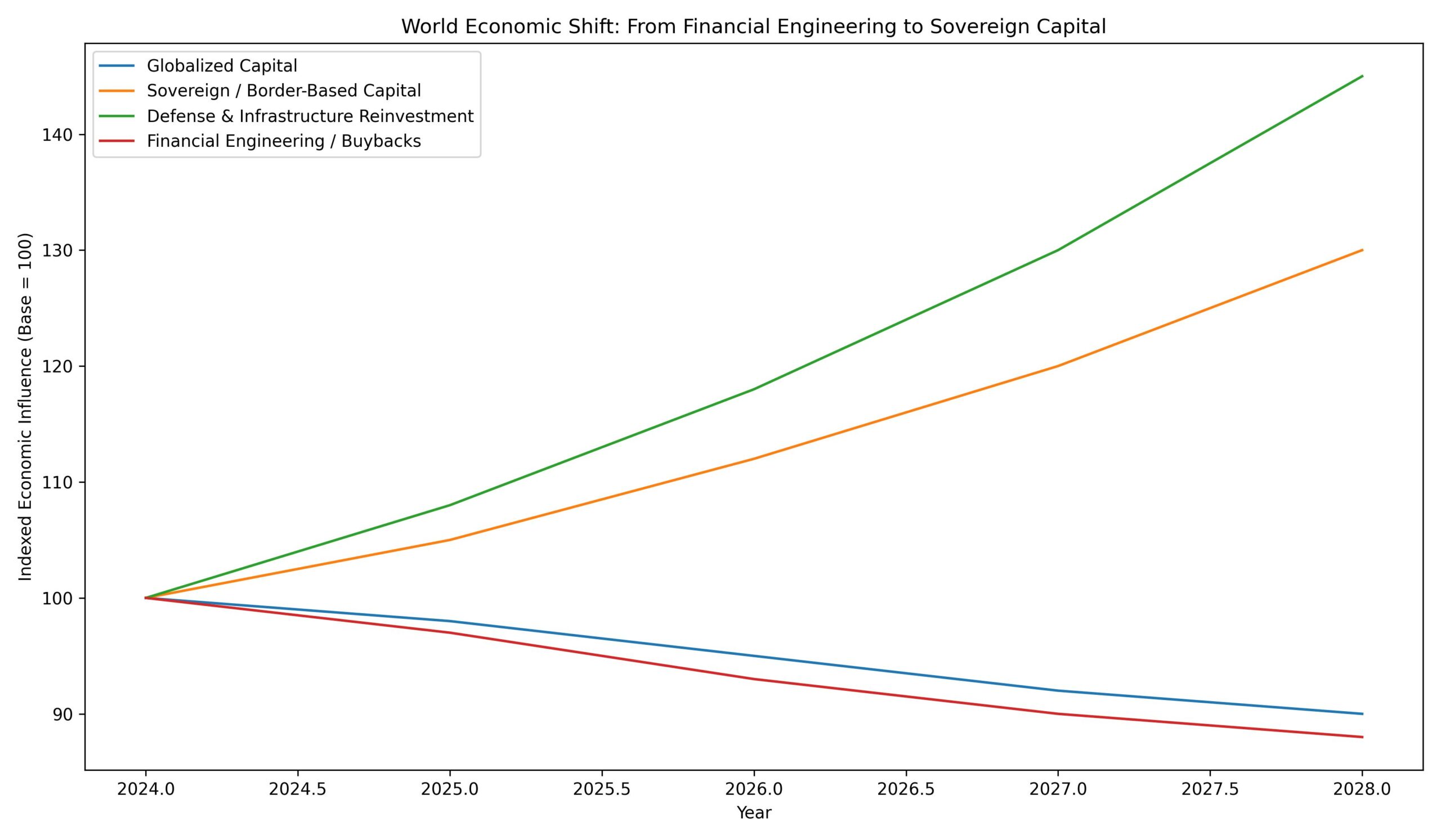

Whether one agrees or not, the implications for markets, defense equities, and global capital flows are enormous.

Stock Buybacks vs. Strategic Capital

For decades, stock buybacks have been a primary driver of equity price appreciation—especially in large defense contractors. Buybacks reduce share count, inflate earnings per share, and reward shareholders without necessarily expanding real output.

Trump’s claim is that this model is no longer compatible with a world defined by borders, military readiness, and supply-chain nationalism.

If defense companies are essential to national security, he argues, then capital should be treated as strategic infrastructure, not shareholder candy. In his view:

- Buybacks weaken long-term production capacity

- Capital should be locked into domestic reinvestment

- Defense firms should align with national objectives, not quarterly EPS optics

From a market perspective, banning or limiting buybacks would compress short-term valuations—but potentially expand long-term enterprise value through real assets, labor, and production scale.

NATO, Borders, and Capital Discipline

Trump’s rhetoric consistently ties NATO obligations to economic accountability. His position implies that countries benefiting from U.S. defense umbrellas must also accept capital discipline—especially in firms that profit directly from military spending.

This reframes NATO not just as a military alliance, but as a capital alliance:

- Defense spending becomes tied to domestic investment

- Cross-border profit extraction is discouraged

- National borders reassert themselves as economic boundaries

In this model, markets stop being purely global and start behaving regionally, with defense, energy, and infrastructure stocks priced based on sovereign alignment, not just revenue.

Greenland, ICE, and Economic Borders

Trump’s repeated references to Greenland—including claims that the U.S. should acquire it “one way or another”—are less about territory and more about strategic assets. Greenland represents:

- Arctic access

- Rare earth resources

- Military positioning

- Control over future trade routes

Similarly, his ICE-related claims frame border enforcement as economic policy, not just immigration control. In this worldview, borders determine:

- Labor flows

- Capital flows

- Tax bases

- Market stability

Markets, in turn, become reflections of who controls land, resources, and movement—not just interest rates.

Will the Stock Market Double?

Trump’s claim that the stock market will double rests on a specific thesis:

- End financial engineering (buybacks)

- Force reinvestment into real assets

- Secure borders and supply chains

- Expand U.S.-aligned territory and influence

- Reprice equities based on production, not leverage

If executed, this would represent a structural reset, not a cyclical rally. Some sectors would suffer short-term shocks—particularly defense, aerospace, and multinational firms—but others could see historic expansion, especially:

- Domestic manufacturing

- Energy

- Infrastructure

- Defense production (not defense finance)

Where BOSSTOX and Boston Made Fit

At Boston Made, the thesis has always centered on real value creation over abstraction—brands, infrastructure, media, education, and long-term systems built for durability, not arbitrage.

BOSSTOX sits at the intersection of this shift: a framework designed to track and communicate value rooted in execution, assets, and ecosystem growth, not just speculative multiples.

If markets move toward:

- Capital discipline

- Domestic reinvestment

- Sovereign-aligned growth

Then platforms that emphasize transparency, structure, and long-term alignment become more relevant—not less.

Final Thought

Trump’s claims—on buybacks, NATO, borders, ICE, and even Greenland—are not random. They form a single economic argument: the era of borderless capital may be ending.

If markets are entering a phase defined by territory, production, and control, then the next decade won’t reward the fastest traders—it will reward the most grounded builders.

Whether the market doubles or not, one thing is clear:

The rules being debated are no longer just financial. They’re geopolitical.

Leave a Reply